5 min read

Highlights:

Every time you click “Pay Now,” a silent digital middleman is making sure your money finds its way.

You’ve probably heard “payment gateway” dozens of times, but what does it actually mean? If you’re building digital payment infrastructure or choosing a provider, understanding this technology matters.

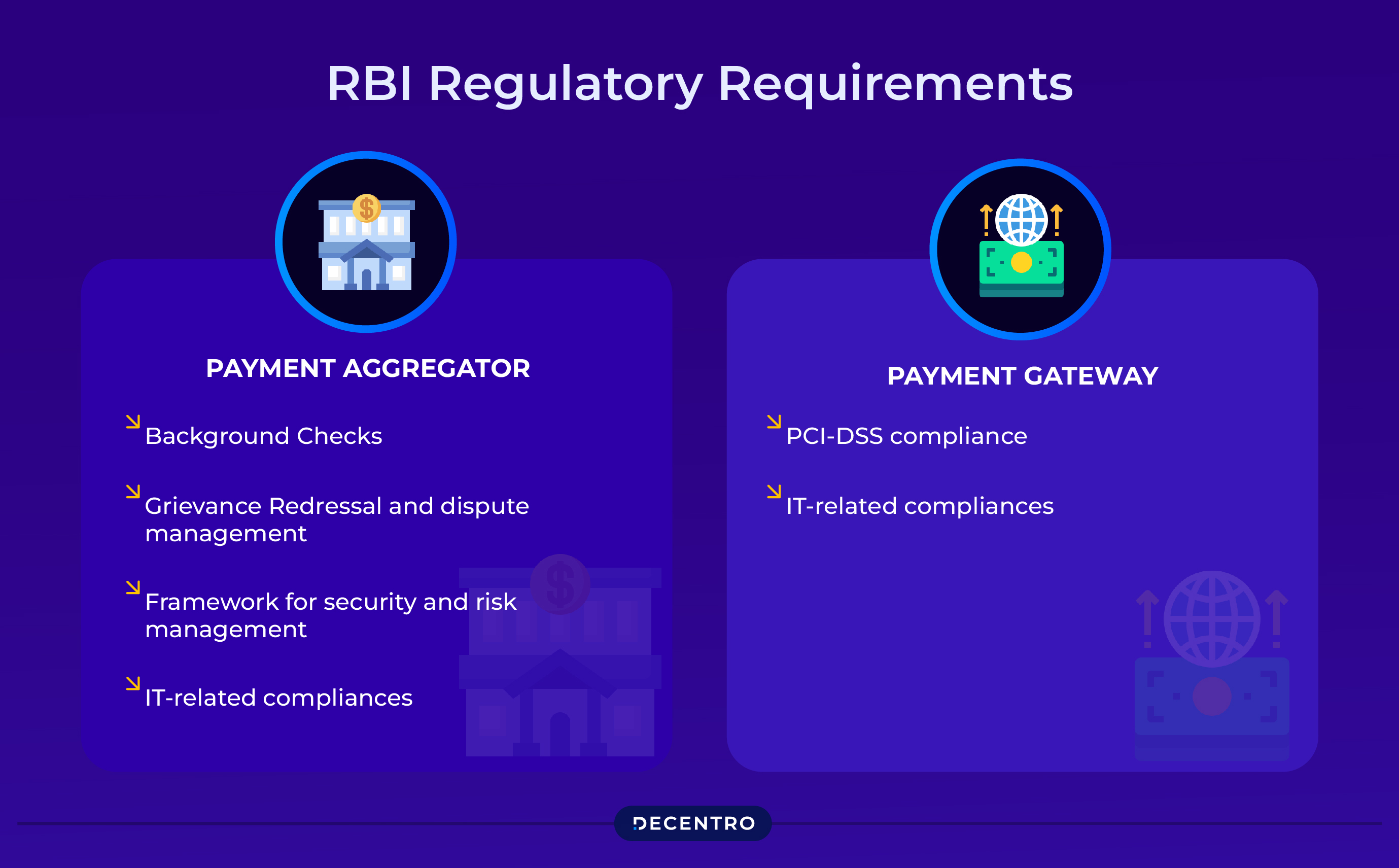

The Reserve Bank of India (RBI) makes a clear distinction between payment gateways and payment aggregators. Gateways provide the technology infrastructure to route transactions, while aggregators handle customer funds and settlement. Understanding this separation is essential for compliance, business architecture, and technical planning.

The RBI defines payment gateways as intermediaries that “act as the bridge between the providers of goods/services (merchants) and those that require them (customers)” to facilitate online payment collection and settlement.

In practical terms, a payment gateway is a technology infrastructure that:

Key distinction: Gateways process data; they don’t touch your money. This matters for regulatory requirements and business liability.

When a customer completes a payment on your platform, the gateway encrypts their data using SSL/TLS protocols, runs real-time fraud checks, and routes the transaction request to the merchant’s acquiring bank. The customer’s bank (issuer) then approves or declines the transaction based on available funds and limits. The gateway receives this response and sends it back to your checkout system. Finally, settlement occurs, moving funds from the issuer to the acquirer—typically the next day.

This entire process completes in 2-3 seconds for successful transactions.

RBI distinguishes these based on fund handling:

| Aspect | Payment Gateway | Payment Aggregator |

| Role | Technology infrastructure to route transactions | Collect, pool, and transfer funds to merchants |

| Fund Handling | No connection to funds | Handles merchant money |

| RBI Authorisation | Not required (voluntary compliance) | Mandatory under the PSS Act 2007 |

| Regulatory Circular | Encouraged to follow baseline tech standards | DPSS.CO.PD.No.1810 dated 17.03.2020 |

For businesses: You integrate with aggregators who use gateway technology. Understanding this separation clarifies compliance responsibilities and technical architecture.

UPI Integration is Critical

India processed 228 billion UPI transactions worth ₹300 lakh crore in 2025, with person-to-merchant payments growing 37% to 67 billion transactions in H1 2025 alone. Without UPI-enabled gateway infrastructure, businesses miss out on over 80% of India’s digital payment volume.

Security and Compliance

PCI-DSS compliance is mandatory for entities that store, process, or transmit cardholder data. Gateways handle this burden—implementing encryption, access controls, and vulnerability management—reducing your compliance scope and breach liability.

Technical Reliability

Modern gateways provide:

This infrastructure would take months to build independently and requires continuous maintenance.

Payment gateways provide the secure technology layer that routes transaction data between customers and banks without handling funds, differentiating them from payment aggregators under RBI regulations.

For Indian businesses, choosing gateway providers with robust UPI integration, PCI-DSS compliance, and comprehensive security features ensures your payment infrastructure scales reliably as digital commerce grows.

1. What’s the difference between a payment gateway and a payment aggregator in India?

Payment gateways provide technology infrastructure to route transactions without touching funds, requiring no RBI authorisation. Payment aggregators handle and pool customer funds before settling with merchants, requiring mandatory RBI authorisation under the Payment and Settlement Systems Act.

2. Do payment gateways need to be PCI DSS compliant?

Yes. All entities that store, process, or transmit cardholder data must comply with PCI-DSS requirements. This involves encryption protocols, secure data storage, regular security audits, and vulnerability management to protect sensitive payment information from breaches.

3. What payment methods can gateways accept in India?

Modern gateways support UPI, credit/debit cards (Visa, Mastercard, RuPay), net banking, and digital wallets. UPI integration is critical—processing 228 billion transactions worth ₹300 lakh crore in 2025, accounting for 84% of India’s digital payment volume.

4. How do payment gateways protect customer card information?

Gateways encrypt card data using SSL/TLS protocols, perform real-time fraud screening, and implement 3D Secure authentication requiring bank verification. Data is tokenised so merchants never store actual card numbers, significantly reducing breach risks and compliance burden.

5. Do I need RBI authorisation to use a payment gateway?

No. Businesses don’t need RBI authorisation to use payment gateways, only to operate as one. You integrate with RBI-authorised payment aggregators or banks that provide gateway services. Payment gateways themselves don’t require authorisation, unlike payment aggregators handling funds.