5 min read

Highlights:

Small business owners often wonder about banking alternatives beyond traditional commercial banks. Cooperative banks offer a unique model—member-owned institutions where customers are also shareholders, built on community welfare principles rather than profit maximisation.

With over 16,000 branches across India, cooperative banking serves rural businesses, traders, and local entrepreneurs through a democratic governance structure. This article explains cooperative banking, how these institutions differ from commercial banks, and their role in India’s financial ecosystem.

Cooperative banking refers to financial institutions owned and controlled by their members, who are both customers and shareholders. Unlike commercial banks, where external shareholders drive profit-driven decisions, cooperative banks operate on the “one-person-one-vote” principle—democratising banking regardless of shareholding size.

As of March 2025, India has 34 State Cooperative Banks operating 2,146 branches, 351 District Central Cooperative Banks with 13,825 branches, and 1,457 Urban Cooperative Banks. This extensive network provides local banking access where commercial bank penetration remains limited, particularly in rural and semi-urban areas.

For business owners, cooperative banks typically offer lower transaction fees, personalised service, and decision-making focused on community development rather than shareholder returns.

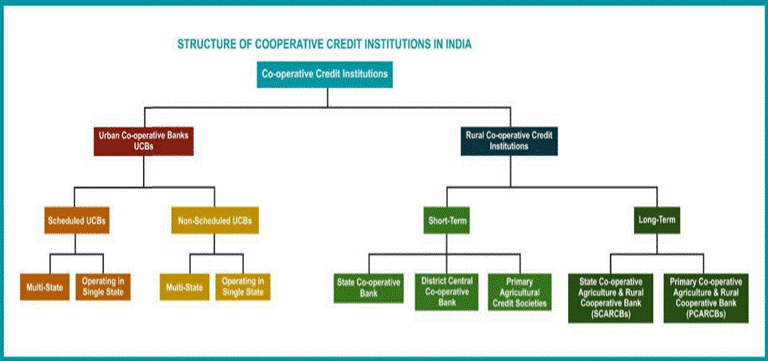

Cooperative banks are categorised into two main types based on geographic focus and customer base:

| Type | Primary Customers | Structure | Services |

|---|---|---|---|

| Urban Cooperative Banks | Traders, SMEs, urban businesses | Single-tier | Business current accounts, trade finance, MSME loans, working capital |

| Rural Cooperative Banks | Farmers, agricultural businesses | Three-tier (PACS → DCCBs → StCBs) | Crop loans, agricultural term loans, farm equipment finance, and rural housing |

Urban Cooperative Banks serve merchants and small businesses in urban and semi-urban areas, providing commercial banking services tailored to local trade needs.

Rural Cooperative Banks follow a 3-tier structure: Primary Agricultural Credit Societies (PACS) at the village level, District Central Cooperative Banks at the district level, and State Cooperative Banks at the state level—enabling agricultural credit delivery across 6.5 lakh villages.

The rural cooperative structure operates through three interconnected levels:

This pyramidal structure ensures rural businesses access credit through local PACS while benefiting from state-level financial resources and regulatory oversight. For business owners in remote areas, this means banking services without travelling to district headquarters.

Cooperative banks operate under dual regulation: RBI governs banking functions (licensing, prudential norms, inspections) under the Banking Regulation Act 1949, AACS, whilst the State or Central Registrar of Cooperative Societies oversees management, governance, and member elections.

NABARD conducts inspections of State Cooperative Banks and District Central Cooperative Banks on the RBI’s behalf, ensuring regulatory compliance for rural cooperative structures.

Banking Regulation Amendment Act 2020, effective 29 June 2020, brought Urban Cooperative Banks and multi-state cooperative banks under direct RBI supervision. For business owners, this regulatory strengthening means enhanced depositor protection (deposits up to ₹5 lakh insured by DICGC), improved governance standards, and greater banking stability.

Cooperative banks play a vital role in financial inclusion, particularly for businesses underserved by commercial banks:

Cooperative banking offers business owners a community-focused alternative to commercial banks, particularly valuable for rural businesses, local traders, and small enterprises seeking personalised banking relationships. With enhanced regulatory oversight post-2020 reforms and ongoing digitisation initiatives, cooperative banks combine traditional community values with modern banking infrastructure.

For SMB owners evaluating banking options, understanding cooperative structures helps identify whether member-owned local banking aligns with your business needs and geographic location.

1. What is the main difference between cooperative banks and commercial banks?

Cooperative banks are owned by member-customers with democratic voting (one person, one vote), focusing on community welfare over profit. Commercial banks are shareholder-owned and profit-driven. Cooperative banks typically serve local businesses with lower fees and personalised service.

2. Are deposits in cooperative banks safe?

Yes. Cooperative bank deposits up to ₹5 lakh per depositor are insured by DICGC. Post-2020 Banking Regulation Amendment, RBI has enhanced supervisory powers over cooperative banks, strengthening depositor protection and governance standards for business accounts.

3. Can I open a business current account with a cooperative bank?

Yes. Urban Cooperative Banks offer business current accounts, working capital loans, trade finance, and MSME credit. Rural cooperative banks provide agricultural and allied business credit. Membership may be required, depending on the individual bank’s bylaws and governance structure.

4. What types of loans do cooperative banks provide?

Urban cooperative banks offer trade finance, MSME loans, working capital, and personal loans. Rural cooperative banks provide crop loans, agricultural term loans (1-25 years), farm equipment finance, rural housing, and non-farm sector credit through NABARD refinance programmes.

5. How are cooperative banks different from scheduled commercial banks?

Scheduled cooperative banks (listed in the RBI’s Second Schedule) can access RBI refinance and maintain government accounts. Non-scheduled cooperative banks operate locally with state registrar oversight. Scheduled banks have stricter capital requirements but broader banking privileges.